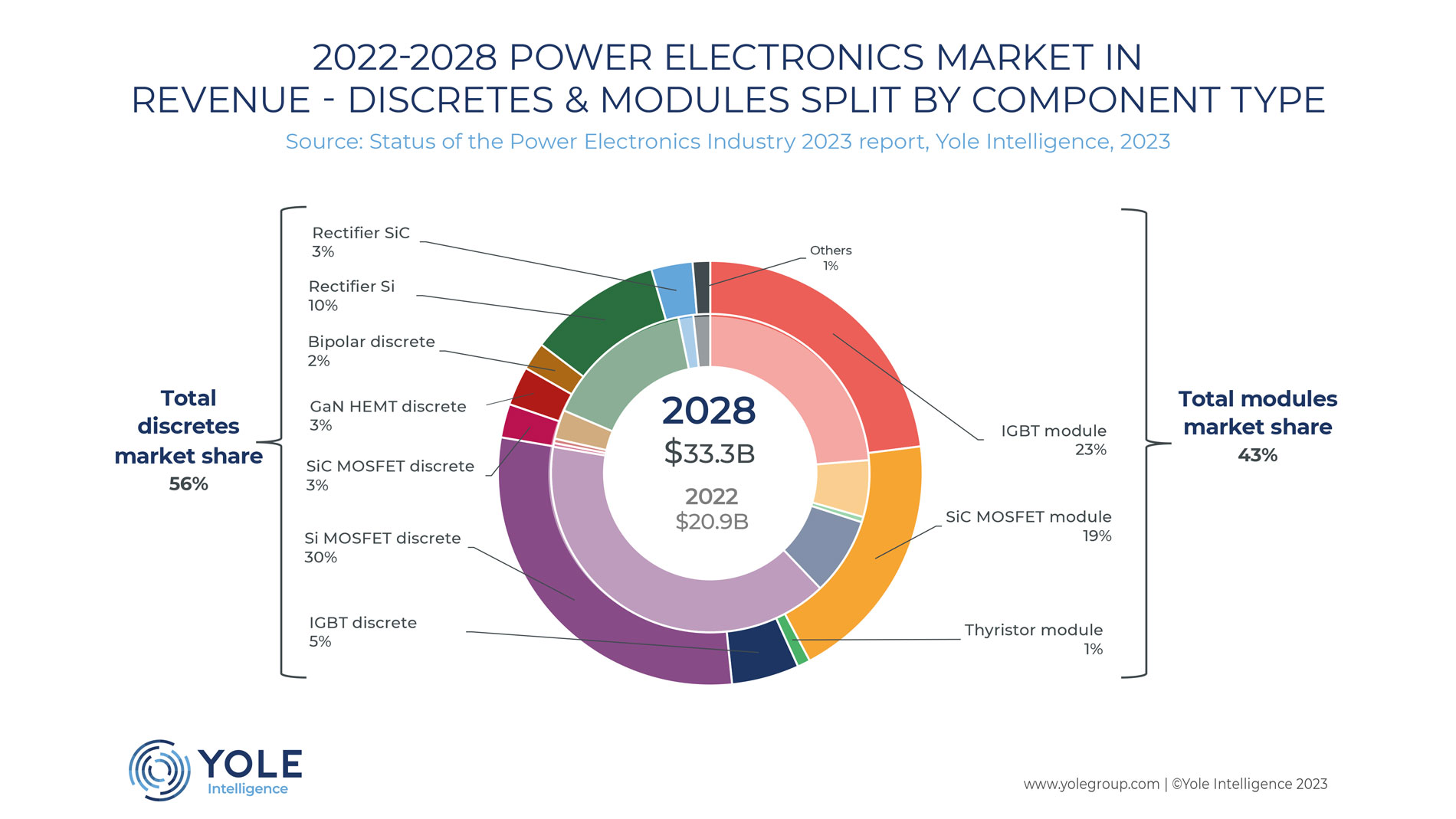

SiC is witnessing substantial growth. The power electronics market for SiC is projected to reach US$ 10 billion by 2029, capturing 28.6% of the global market. This is being driven by technological trends like 200 mm platforms, higher power densities, and optimized power module packaging. The trends are supported by a shift towards vertical integration within the SiC ecosystem. Leaders like STMicroelectronics, ROHM, onsemi and Wolfspeed, for example, are enhancing their supply chains to include internal substrate production capabilities. Meanwhile, there has been a tremendous effort in expanding the SiC wafer capacity, especially by Chinese players such as Tankeblue, SICC, SemiSiC and numerous others.

GaN technology is also showing robust growth across multiple applications, including consumer electronics and automotive, particularly in areas like fast chargers and overvoltage pro-tection, as well as in power supply applications in home appliances and data centres. Innovation is also driving the exploration of the next generation of semiconductors, like bulk GaN, gallium oxide, and diamond.

Automotive electrification transforms power module technology and market trends

Electric vehicles (EVs) have already gained considerable market acceptance and represent a significant share of the overall power electronics industry. In 2023, almost 30% of all passenger vehicles sold globally were electric. This percentage is expected to increase in the coming years, with the projection that EVs will make up 50% of all passenger vehicles by 2028.

EVs represent a significant and sustainable market opportunity, but they also have a much wider impact. The automotive industry has a reputation for driving standards and introducing new technologies in power electronics. The immediate motivation is to improve driving range and to lower costs. But the advances have repeatedly altered trends in power module technologies and the development of battery packs, and streamlined supply chains. This then creates new opportunities as the technology is adopted in various industrial applications requiring robust performance and enhanced efficiency.

The impacts of the trend toward more affordable EVs

EVs are entering a new phase of market expansion, commonly referred to as the ‘move towards more affordable vehicles.’ Following the initial rush towards highpower, longrange vehicles, vehicle manufacturers are broadening their customer base to include those seeking EVs in the US$20,000 to US$25,000 price range. This involves various strategies for cost reduction, such as reducing electric motor drive power, downsizing onboard charger power, decreasing battery capacity, increasing system integration, and reducing the SiC content in vehicles. These trends are impacting the EV supply chain, with different strategies emerging in China than in Europe and the United States.

The performance and cost dynamics of SiC

Even as affordable EVs look for ways to use more silicon, the automotive sector is still forecast to dominate the demand for SiC devices for the foreseeable future. SiC made its breakthrough in the Tesla Model 3, and enjoys widespread use in 800 V battery electric vehicles (BEVs), which are expected to account for nearly 80% of the market. Major manufacturers, like Tesla and BYD, are increasing their use of SiC tech-nologies, with BYD also developing in-house SiC capabilities and collaborating with other semiconductor firms for SiC supply.

There are cost considerations associated with the adoption of SiC technology. But recent ca-pacity expansions in both SiC wafer and device technology, as well as advances in packaging techniques, and market dynamics are driving down costs and making SiC technology more accessible to a wider range of applications.

Smart integration is about more than size

Cost reduction is also a fundamental driver of smart integration in power electronics. The main focus is on minimising energy waste, and maximising on the potential of renewable energy, to ultimately reduce environmental im-pacts. Smart integration does this at all levels of the energy ecosystem, by exploiting possible synergies between the different applications in generation, distribution, energy storage, and consumption. It is being applied to interconnect everything from wind, wave and photovoltaic systems, to battery storage or hydrogen pro-duction systems and the grid, as well as to do-mestic, e-mobility and industrial consumption.

This trend influences a range of technological developments needed to reduce the size and cost of solutions, to ease deployment and foster adoption. Encompassing everything from liquid cooling to WBG technologies, solutions require development across multiple domains, thus challenging developers with diversifying their areas of expertise, and organisations with exploring new business opportunities to offer complete solutions. In this sense, smart integration is reshaping supply chains, and mergers and acquisitions are to be expected.

Challenges and forecasts

As capacity expansions, particularly in SiC, come online in 2024, there is a potential that supply constraints will ease. This will encourage significant growth and market opportunities across not only automotive but also industrial and energy sectors, which will in turn drive further adoption of power electronics technologies. Yole Group is an international company recognized for its expertise in the analysis of markets, technological developments, and supply chains, as well as the strategies of the leading players. Visit Yole Group at the PCIM Europe – or online all year round –to share its insights on trends in power electronics.

Yole Group is presenting its findings on a number of topics at the conference:

- “Revolutionizing Power Semiconductors: Decade of Transformation and Future Trends”, on the Technology Stage, 11 June 2024, 12:20 p.m.

- “How automotive electrification is trans-forming power module technology and market trends.” on the E-Mobility & Energy Storage Stage, 13 June 2024, 12:05 p.m.

- “How will the trend toward ‘more affordable vehicles’ Impact EV technologies and the supply chain?” on the E-Mobility & Energy Storage Stage, 11 June 2024, 12:05 p.m.

- “Catalyzing the Future: Unveiling the Performance and Cost Dynamics of SiC Power Technology” on the E-Mobility & Energy Storage Stage, 12 June 2024, 12:05 p.m.

- “Smart integration is more than just making systems more compact.” on the Smart Power System Integration stage, 13 June 2024, 12:40 p.m.