Power SiC growth picks up pace, driven by auto, industrial, and AI

9 Jun 2026

A new growth phase with 800V BEVs, renewable energy, data centers, as well as global investments in a 200mm platform, demonstrate that SiC remains the key enabler for the next generation of power electronics.

By Poshun Chiu, Principal Analyst, Compound Semiconductors and Ahmad Abbas, Compound Semiconductors analyst, Yole Group

The power SiC market is entering a strong growth cycle, supported by accelerating electrification trends and continuous improvements across the value chain. With a forecast market value of $11 billion by 2031 and a 20 percent CAGR (2025–2031), SiC is establishing itself as a key enabler of next-generation power electronics. From wafers to devices, the ecosystem is evolving rapidly, driven by both technological advancements and structural shifts in supply and demand. Yole Group unveils the latest insights from its annual report, Power SiC 2026. Discover the key highlights in this snapshot!

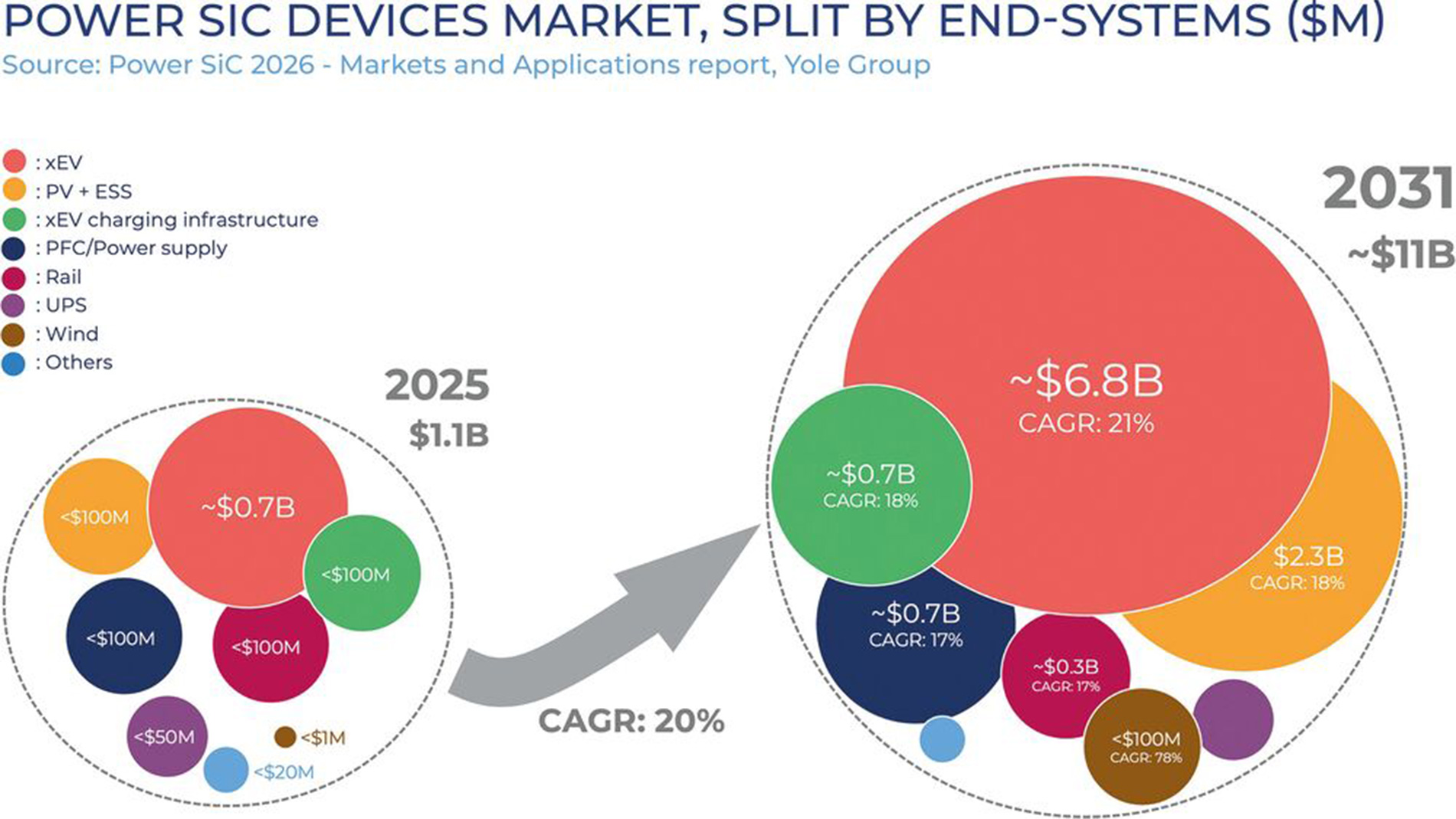

Starting at $1.1 billion, the global market for SiC applications is expected to grow to approximately $11 billion by 2031. The key drivers of this growth are electric vehicles, charging infrastructure, and photovoltaic and energy storage applications. (Image: Yole Group)

Automotive Leadership Meets Diversification: The Engines of SiC Growth

Automotive remains the primary driver of power SiC growth over the next five years. The recovery in automotive demand is fueled by the rapid deployment of 800V battery electric vehicles (BEVs), in which SiC is the main choice. While 400V architectures still dominate with more than 80 percent market share in 2026, the transition toward 800 V and even 1000 V platforms is accelerating. By 2031, these high-voltage architectures are expected to penetrate more than 50 percent of the market, with nearly one in two BEVs integrating 800 V or 1000 V systems.

This shift is largely driven by Chinese OEMs which are leading the rollout of high-voltage platforms, supported by expanding charging infrastructure and declining SiC substrate costs. As a result, automotive will continue to fuel SiC demand.

At the same time, diversification is underway. Indeed, applications such as photovoltaic systems combined with energy storage, EV chargers, and power supplies, including those for AI datacenters, are expected to grow at a double-digit CAGR. Power supplies for datacenters are forecast to be a multi-hundred-million-dollar market for SiC over the next few years.

Scaling the Ecosystem: Vertical Integration, 200 mm Transition, and Global Competition

The SiC supply chain is undergoing a significant transformation. As of 2026, vertical integration remains the dominant strategy among leading IDMs such as STMicroelectronics, onsemi, Wolfspeed, and Rohm. These players are strengthening internal wafer capabilities while accelerating the transition to 200mm manufacturing platforms. In parallel, some key IDMs, such as Infineon and Bosch, are working with external wafer suppliers to better focus on the device level.

Shipments by SiC wafer and epiwafer suppliers grew significantly, in line with the increase in SiC demand. SICC, TankeBlue, EpiWorld, and TYSiC are gaining market share.

While supply chain control remains strategic, constraints have eased compared to previous years.

The transition to 200mm wafers represents a major inflection point for the industry. High-volume production is already underway at companies like Wolfspeed, Infineon Technologies, and Bosch, with many others expected to follow between 2025 and 2026. More than ten fabs have been announced globally, with future capacity expansions largely centered on 200 mm platforms, while 150 mm growth is expected to slow from 2026 onward.

China’s Rise in SiC: From Local Demand to Global Supply Influence

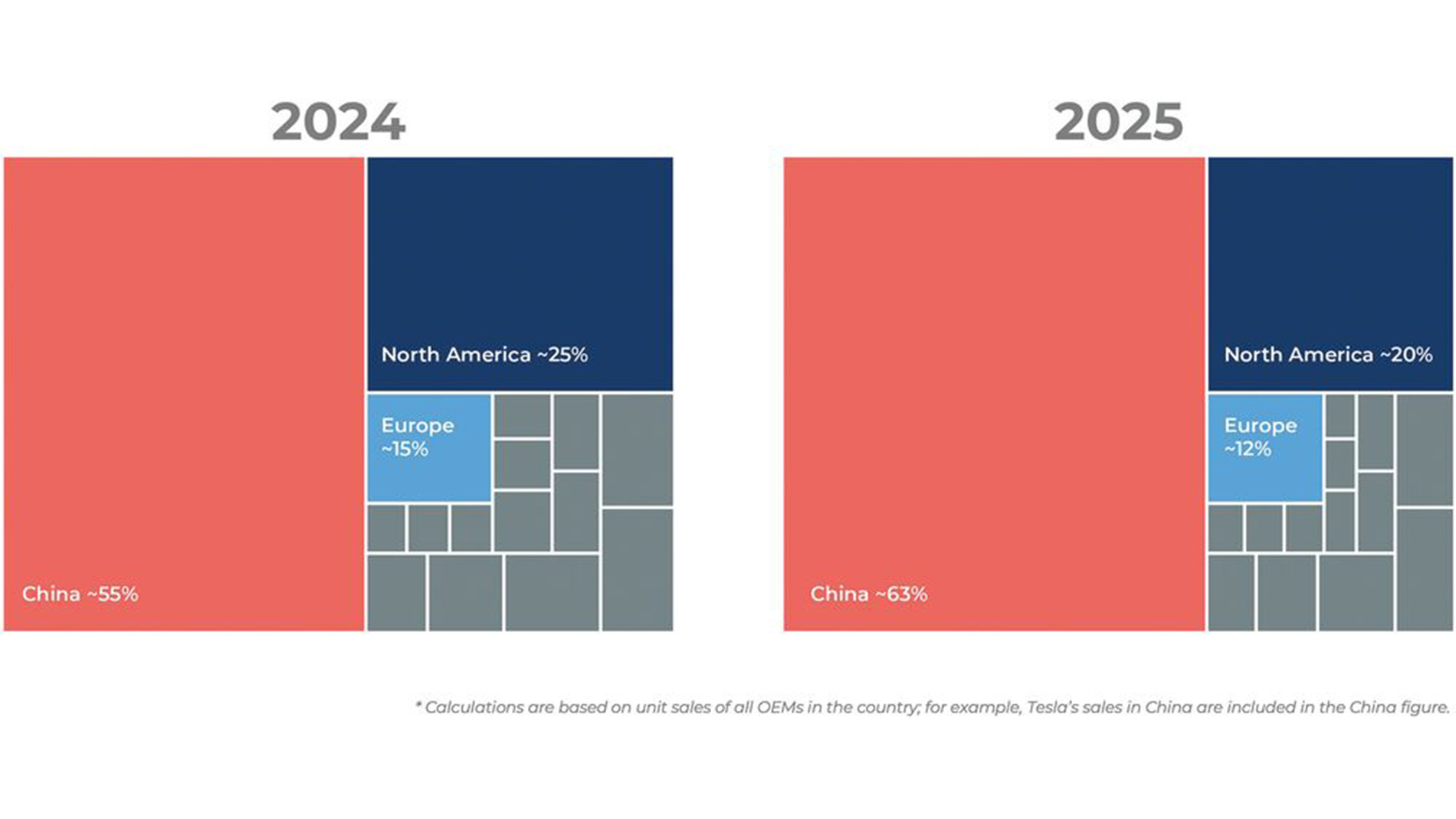

China is rapidly strengthening its position across the SiC ecosystem, emerging as both a key demand driver and a major supply hub. In 2025, China accounted for more than 60 percent of the SiC-based BEVs. Local players such as SICC and TankeBlue have captured significant wafer market share, while companies like UNT are expanding their presence in device manufacturing. This growth is fueled by strong domestic OEM demand. Chinese OEMs shipped high volumes of SiC-based BEVs in 2025, almost comparable to the Tesla shipments. As a result, a dual strategy is emerging across the industry: supply chain localization combined with global sourcing to mitigate geopolitical risks and capture international opportunities.

Chinese market remains the driver for SiC BEVs in 2025. (Image: Yole Group)

Technology and Manufacturing Trends: The 200mm Inflection Point and innovation

Technological evolution is closely linked to manufacturing scale. The shift to 200 mm wafers is enabling improved cost efficiency and higher production volumes, supporting broader SiC adoption. At the same time, players across the value chain are moving downstream to capture additional value.

While 200 mm is becoming the next major manufacturing platform, innovation on 300 mm SiC substrate continues, though it remains in its early stages. Since 2024, multiple demonstrations have appeared, particularly from Chinese suppliers such as SICC. The first targeted applications are mainly outside of power electronics, such as AR/VR glasses and advanced packaging. For power devices, some R&D on specific process steps is still under development.

On the device side, planar and trench SiC MOSFETs are expected to coexist, while trench architectures continue to gain momentum through players such as Infineon, Bosch, Rohm, with more to come. The industry is also expanding beyond traditional voltage classes toward 6.5 kV and 10 kV devices, while JFETs and Super Junction MOSFETss are emerging. In addition to packaging, some companies are exploring the embedded concepts in Power SiC.

“Beyond SiC MOSFETs, the power SiC device landscape is becoming more diversified, with JFETs, Super Junctions, and higher-voltage devices emerging to address more specific performance and application requirements.”

The power SiC market is transitioning from a phase of early adoption to large-scale deployment, driven by automotive electrification and expanding industrial applications. With strong growth expected through 2031, the industry is being reshaped by technological advancements, supply chain strategies, and regional dynamics. »Beyond SiC MOSFETs, the power SiC device landscape is becoming more diversified, with JFETs, Super Junctions, and higher-voltage devices emerging to address more specific performance and application requirements.

“The power SiC market is transitioning from a phase of early adoption to large-scale deployment, driven by automotive electrification and expanding industrial applications.”

The rise of 800V architectures, the transition to 200 mm manufacturing, and the increasing role of China are redefining the competitive landscape. At the same time, continued investments, exceeding 30 billion dollar globally, highlight the strategic importance of SiC in the future of power electronics. In this rapidly evolving environment, success will depend on the ability to scale efficiently, secure supply, and position strategically across the value chain. eg